Flexible and Efficient Probabilistic PDE Solvers through Gaussian Markov Random Fields

Fast probabilistic counterparts to numerical PDE solvers, powered by SPDEs & sparse linear algebra.

Fast probabilistic counterparts to numerical PDE solvers, powered by SPDEs & sparse linear algebra.

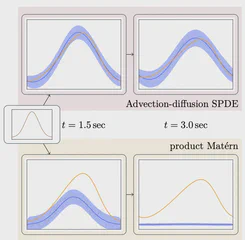

Introduces GP-FVM, a probabilistic counterpart to the finite volume method, enabling large-scale probabilistic PDE simulations.

Fast, flexible and user-centered Julia package for Bayesian inference with sparse Gaussians

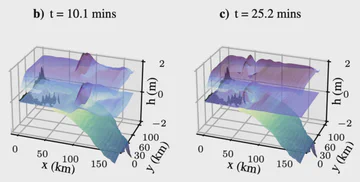

MSc Research Project. A case study on the shallow-water equations.

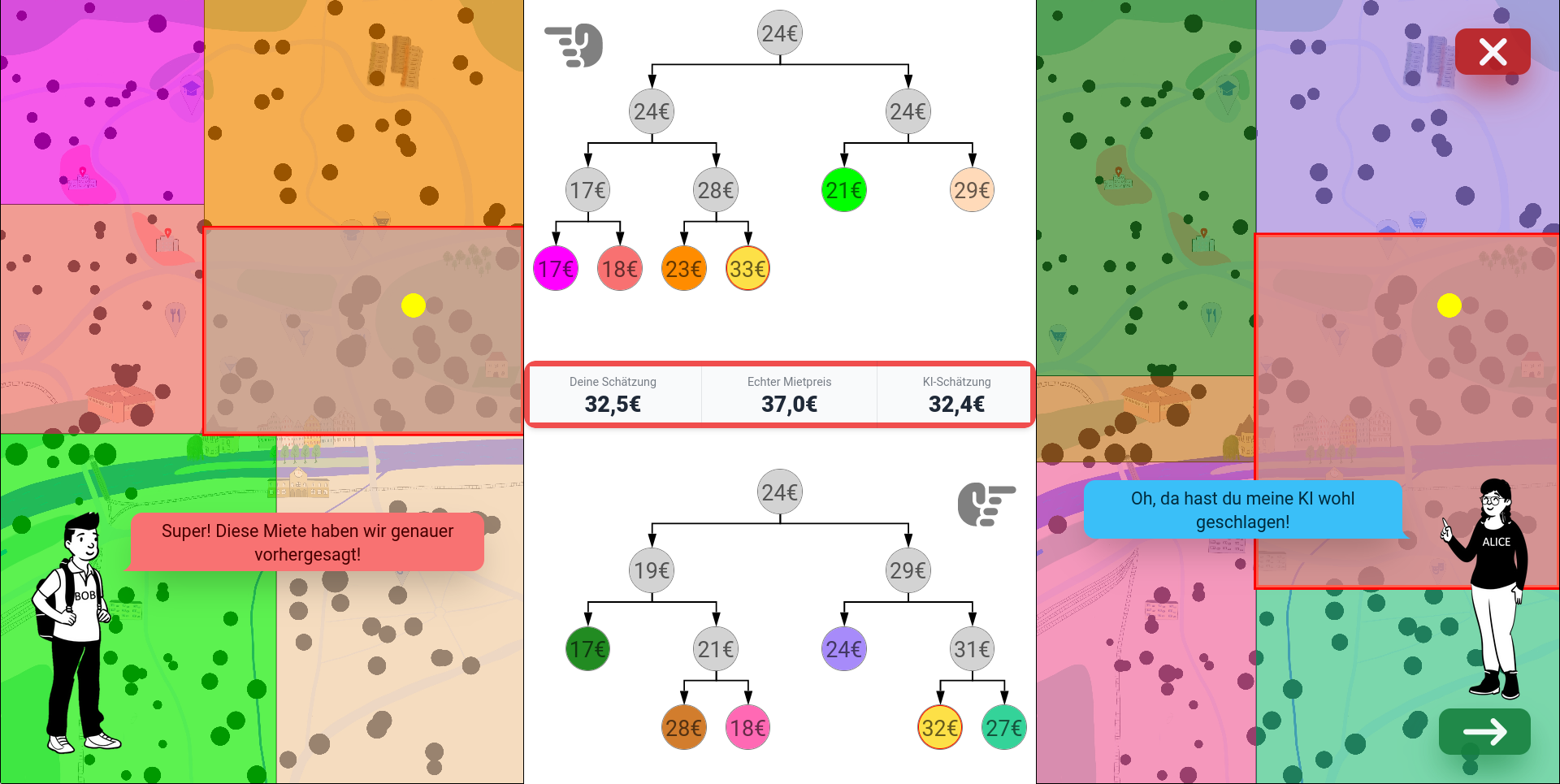

Teaching people about machine learning by predicting apartment rents with decision trees.